The EV Mania (Part 2 of 3)

Understanding the EV manufacturing and supply chain and prospects for "Made in India" electric vehicles

To join the mailing list for Indian Energy Quadfecta, click Subscribe and never miss an issue!

Welcome to another edition of Indian Energy Quadfecta. We are following up a snapshot on Electric Vehicles in India with the second of our three part series, this time focused on EV manufacturing and supply chain.

The Battery Puzzle

A successful transition to lower carbon transportation in India will require more than just customer adoption of EVs, but also a robust domestic supply chain that can ensure this transition is durable. Ultimately, the promise of EVs in India isn't just about getting greener cars on the road, but also about where they are made and how they are sourced. Developing domestic elements of the EV supply chain will ensure that economic 'ripple effects' accrue to the benefit of the broader economy, not just the select consumers who are early adopters of EVs in India. When we speak of the EV supply chain, arguably the most critical component is the battery, which is of course crucial not just for the deployment of EVs but also utility scale renewable power generation more broadly. The success case of a robust manufacturing base for batteries is nothing short of incredible: the IEA estimates that India will be the single largest market for battery technology in the world by 2040 as EV adoption and renewables in the power sector grow significantly.1 Serving much of this explosive battery demand through domestic production could be transformative for the country's manufacturing sector. On the other hand, not doing so would mean India may simply be substituting one type of import addiction with another; instead of being heavily reliant on foreign oil it would be heavily reliant on foreign batteries.

Breaking Down the Supply Chain

But what do we really mean when we say 'battery production'? To help understand the various components of the supply chain, the chart below from Yole Developpement provides a helpful illustration.

Each component of this interconnected supply chain can introduce a further web of complexity, so for our purposes, it is most useful to think of battery production in terms of three simple categories:

Upstream - involves mining and extracting the metals which are inputs to the battery (lithium, nickel, manganese, cobalt, copper, graphite etc.)

Midstream - involves production of key battery components (separators, anodes, cathodes, electrolytes)

Downstream - involves production of battery cells and packs which will ultimately be assembled and used in battery systems (e.g. EVs or utility scale storage)

Across this battery production chain, the global market today features a clear leader: China. With key upstream relationships globally and heavy historical investments in domestic midstream and downstream capabilities, China today accounts for over 80% of global cell manufacturing capacity.2 Chinese dominance in this space is increasingly being challenged by Europe and the U.S., but India - ranked 18th in the world in the Bloomberg New Energy Finance Li-ion battery supply chain ranking - is not in the running as of yet.3

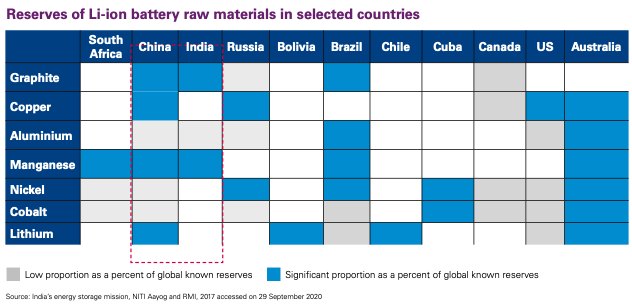

A key limiting factor for India's battery supply chain is simply a lack of domestic raw material reserves: India has notable reserves of graphite and manganese, but it lacks the other critical elements for Lithium-ion batteries such as lithium, cobalt, and nickel.4 This issue is not just relevant for lithium-ion batteries - which remain dominant today - but also novel alternate battery chemistries (e.g. solid state batteries) which are still reliant on lithium and other metals.

While lack of domestic reserves will pose a challenge for India, China's (and to some extent Japan and South Korea's) success in cell refining and manufacturing demonstrates that world-beating manufacturing capabilities can still be built while sourcing metals from abroad. The upstream battery game will naturally be an uphill battle for India, but midstream and downstream battery production, along with battery disposal and end-of-life recycling present significant opportunities for domestic growth. Moreover, the localization of battery production in India must graduate beyond just assembly of battery packs to full scale cell manufacturing in order to capture more of the value chain over the longer term. In the meantime, growing EV adoption too quickly in India without commensurate investments in the domestic supply chain could actually do more to bolster China's manufacturing sector more than India's own.

Buzz and Activity

In an effort to promote much-needed local manufacturing, the Indian government has rolled out a number of incentives targeting various aspects of the value chain. The latest cabinet approved an INR 26,000 crore (US $3.5bn) production linked incentive (PLI) to incentivize EV production,5 along with an INR 18,000 crore (US $2.4bn) PLI to incentivize battery manufacturers to manufacture locally and partially offset the high up-front capital expenditure requirements.6 In terms of domestic production activity in the private sector, some promising signs have emerged over the last 6-12 months including:

Last week, Tata Motors (with investments from TPG and ADQ) announced a $2bn investment plan solely dedicated to EV production over the next 5 years

Ola Electric announced it is in the process of setting up the world's largest electric scooter factory, with the ability to manufacture 2mm electric scooters annually, growing to 10mm at full capacity (this would represent 15% of total global e-scooter production!)

Tesla had a much publicized entry into India in January when it set up an Indian subsidiary, with plans to build a manufacturing facility. These plans have not yet been operationalized due to high import duties India levies which substantially boost the cost of an EV (Elon Musk expressed as much on twitter), but the news has generated buzz nevertheless

A growing chorus of EV and battery manufacturers such as Ather Energy, Amara Raja, Lucas TVS, have announced plans to scale manufacturing of EVs and battery components over the next 5-7 years

Realizing India's transport electrification objectives will require many more such commitments across a number of private and public sector participants. In addition to domestic new-build production capacity, India will also require substantial development of its battery recycling capabilities, including large-scale Lithium-ion recycling plants as well as urban mining (the practice of recovering raw materials from electronic waste - of which there is plenty in India - found in urban landfills). Ultimately, developing these domestic manufacturing capabilities, despite some natural limitations on domestic raw material availability, may well be the key to unlock the EV revolution in India.

Up Next…

Stay tuned for the next issue of Indian Energy Quadfecta, where we will round out our mini series on electric vehicles by focusing on the infrastructure side of the EV market.

To join the mailing list for Indian Energy Quadfecta, click Subscribe and never miss an issue!

IEA (January 2020), https://www.iea.org/commentaries/india-is-going-to-need-more-battery-storage-than-any-other-country-for-its-ambitious-renewables-push

Bloomberg New Energy Finance (October 2021), “U.S. Narrows Gap With China In Race To Dominate Battery Value Chain”, https://about.bnef.com/blog/u-s-narrows-gap-with-china-in-race-to-dominate-battery-value-chain/

Bloomberg New Energy Finance (October 2021), “U.S. Narrows Gap With China In Race To Dominate Battery Value Chain”, https://about.bnef.com/blog/u-s-narrows-gap-with-china-in-race-to-dominate-battery-value-chain/

KPMG, October 2020, “Shifting gears: the evolving electric vehicle landscape in India,” https://assets.kpmg/content/dam/kpmg/in/pdf/2020/10/electric-vehicle-mobility-ev-adoption.pdf

India Today, September 2021, https://www.indiatoday.in/auto/latest-auto-news/story/cabinet-clears-rs-26-000-crore-incentive-scheme-to-boost-electric-vehicle-production-in-india-1853090-2021-09-15

Hi Sankalp, very interesting read of your article on the key subject that is talked about so much.

Having read few articles from different publications, i thought I would share my observation of a couple of points that may be of interest to you.

I read that the overall load on electricity requirement to meet energy requirement of 80% of global EV would only increase by 15%. If these theoretical estimates are to be believed, then the burden on electricity generation may not be too much an issue in India?

Secondly, your view on heavy reliance of battery importation equalling current reliance on oil imports .. If the energy requirement of EV is estimated to be 1/3rd of fossil fuel, the overall import cost therefore would be reduced?

Would love to hear your views on the above observations.

All the best,

Damodar