The 'White Gold' Rush for Lithium: India's Entrance and Inference

India's discovery of a 5.9mm ton lithium deposit in Kashmir earlier this year could be a game-changer. But for now, they are just "inferred resources". What happens next?

The global race for lithium - one of the critical metals powering EV batteries - saw a welcome entrant earlier this year when India discovered a 5.9mm deposit in the Reasi district in Jammu & Kashmir (J&K). Representing ~5% of the current global lithium market, this additional supply could be a meaningful needle-mover. But there are a lot of steps to be taken in the interim. So what happens next? This is the subject of this week’s Indian Energy Quadfecta. Here are 6 takeaways in 60 seconds:

6 Takeaways in 60 Seconds

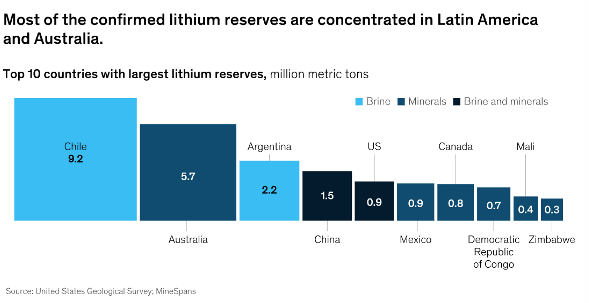

A Game-changer in Waiting: With EV sales slated to grow rapidly around the world - including a ~90% targeted CAGR in India through 2030 - discoveries of battery metals like lithium are welcome news. If the recent 5.9mm deposit in Kashmir is ultimately realized, it would represent ~5% of the current global market, and India would join as a significant supply source behind Chile, Argentina, Bolivia, Australia, and China.

Mineral Nationalism: As the race for Lithium (aka “White Gold”) heats up, countries are acting predictably territorial. The president of Chile announced this week that it will be nationalizing lithium mines, Mexico nationalized its reserves earlier this year, Indonesia similarly restricted exports of Class I nickel in 2020. Expect new discoveries of battery metals to continue to be carefully guarded.

Miles to Go: The lithium deposits in Jammu & Kashmir is classified as “lithium inferred resources,” which signals there are many remaining steps before we know its true quality and recoverability. Required prospecting, test drilling, resource definition, feasibility studies means it could be years - even a decade - before recoverable lithium is extracted.

Climbing Up the Value Chain: The real economic prize for lithium extraction lies not just at the mine site, but further downstream. Simply exporting unprocessed natural resources leaves way too much value on the table. The need of the hour is significant expansion in domestic lithium processing and refining capabilities in India alongside mining.

The Cost Question: All else equal, a domestic lithium source of this scale will meaningfully decrease battery production costs. But “all else” is rarely equal. Whether the lithium from the J&K site will be economically recoverable is an open question. The answer will depend on the lithium concentration within a high confidence interval, and the ability to separate the lithium from other metals like bauxite.

Ecological Concerns: Reasi District - like many parts of J&K - sits within an ecologically sensitive zone. Some local community members are already apprehensive about anticipated relocations and the impact on the surrounding environment from large scale lithium mining. Plans for remediation and community support will need to be developed concurrently with the project.

A Deeper Dive

Lithium 101

Before we dive further, let’s review some need-to-knows about Lithium.

A critical component of a critical component: With batteries representing up to 40% of the cost of EVs, and raw materials accounting for 77% of the cost of these lithium ion batteries, it is no surprise that lithium is often referred to as “white gold”. In a future that is increasingly electric, control of these battery metals will be analogous to controlling oil today.

Scarcity in abundance: Lithium is the lightest and technically the most abundant metal on the planet. However, extracting lithium in the right concentrations, and in a way that is economically feasible is a challenge. Moreover, it’s not just about finding enough lithium, but also the pace at which we find it. With battery demand projected to grow 6-7x by 2030 globally - including a 90%+ CAGR targeted for EVs in India through 2030 - the supply side has to deliver at record speed.

Guesstimates to Estimates: As with any type of mining, the evolution from reserves to actual production is filled with uncertainty and educated guesses. The process from initial reconnaissance to actual development take years, sometimes decades. Over the course of this time, geologists and mining engineers delineate what they think could be in the ground, what they think realistically is in the ground, what is actually in the ground, and how much of what is in the ground can one economically extract.

Two major sources: Lithium is extracted today in two major forms: brines and hard rock mining. With brines, lithium is found naturally occurring pools of saline groundwater which are pumped to the surface in successive ponds and then evaporated to recover lithium salts. With hard rock mining, lithium is recovered from hard rock units called pegmatites which include water and concentrated minerals. These pegmatites include lithium-bearing components known as Spodumene. Lithium extraction from brines occurs often in the Latin American deposits across Chile and Argentina, whereas hard rock mining is common in Australian deposits, among other locations.

Two Major Compounds: Whether sourced from brines or hard rock, the lithium input for lithium-ion batteries are typically in the form of two compounds: Lithium carbonate and lithium hydroxide, with the later often preferred by automakers seeking higher energy density. Lithium carbonate is also sometimes used as an intermediate to be later converted to lithium hydroxide.

A Critical Discovery of A Critical Material

Simply put, the discovery in J&K could be a big deal (emphasis on could). In terms of volumes, the estimated 5.9mm metric ton deposit alone represents over 5% of the current lithium market globally. It also represents the first major discovery of the critical battery metal in India, the previous one being a small ~1,600 metric ton deposit found in Karnataka in 2021.

With relentless growth in the EV market, a sizeable domestic source of lithium is a meaningful needle-mover. India currently imports all of its Lithium from abroad ,which amounted to $3.4bn over 2018-21. A domestic source of this magnitude could help India achieve its EV adoption targets and its Atmanirbhar (“self reliance”) aspirations.

Current global lithium supply is dominated by a handful of countries - Chile, Australia, Argentina, China (see below) - and India would benefit from joining the club.

Mineral Nationalism

Given the central role of lithium in an increasingly electric world, securing access to these battery metals is a geopolitical imperative as much an economic one. India’s recent discovery should therefore also be looked at in the broader context of mineral nationalism seen around the world. Chile - the largest source of lithium reserves in the world - has been signaling that it will nationalize its lithium industry; President Boric confirmed this again earlier this week. Similarly, Mexico nationalized its lithium deposits earlier this year. Indonesia did the same with its exports of Class I Nickel - another battery metal - and has also been viewed as exploring an OPEC-style bloc for these resources.

Even in the U.S., which is currently not among the major suppliers of lithium, there is a significant push to ‘insource’ as much of the battery value chain as possible. The much discussed Inflation Reduction Act (IRA), for example, stipulates battery manufacturers must source 40% of the value in their batteries domestically or from free trade partners.

Given the broader geopolitical climate around battery metals, we should expect the J&K lithium discovery to be similarly treated with a keen eye on the Indian national interest.

Still Early Days

It’s important to acknowledge that the process going from exploration to development is a long and often circuitous one. As of now, the J&K resource is far from extractable. Its technical term is “Lithium inferred resources” according to the Geological Survey of India.

One can think about the exploration, development, production process in stages. A simplified 7 step process is illustrated above, and the current status of the lithium project in J&K seems to be somewhere around the prospecting stage which is still in relatively early exploration. In mining industry terms, we are currently in the ‘G3’ exploration phase, and need to get to G2 and then G1 before being ready for the feasibility study. This process will almost certainly take several years.

Some additional detail around the various stages described above:

Reconnaissance: Initial stage of exploration, where geological surveys, satellite imagery, etc. are used to identify areas with potential. For lithium, it involves finding features and mineralization that are indicative of deposits, such as salt flats, evaporite basins, and pegmatite rocks.

Prospecting: More detailed geological mapping, fieldwork, and sampling to confirm presence of lithium and estimate the size + grade of the deposit. Involves analyzing rock samples, and using geophysical surveys to determine the depth of the deposit.

Exploration drilling: Further assesses the size, quality, and continuity of the deposit. Involves drilling and analyzing core samples to determine the lithium content and other mineralogical characteristics.

Resource definition: Defines size and quality of the deposit in more detail. Involves estimating the mineral resource and reserve, and the mining method and processing technology that will be required to extract the lithium.

Feasibility study: A key milestone pre-development. Study determines the economic viability of the extraction project. Includes testing the quality and purity of the lithium, estimating cost of production, and assessing environmental impact.

Development: If the feasibility study supports development, next stage includes financing and permits, and infrastructure development for mining and processing.

Production: Post development, the final step commercial production of lithium, which can take several years depending on the size and complexity of the project.

Eye on the Prize: Going further up the battery metal value chain

Access to domestic mine sites is certainly a boon, but perhaps the real game for economic prominence is played further up the value chain. For example, China - the undisputed king of the global battery value chain - mined less than 14% of the world’s lithium, but controls 44% of lithium chemical production, 78% of cathode material production, and 70% of battery cell manufacturing. Control of the downstream value chain matters. This means building up lithium refining and processing capabilities at scale, which takes time, capital, and technical know-how.

This dynamic is of increasing importance to a number of African countries as well. In the African continent, an estimated ~70% of exports are unprocessed metals, for which refining and processing is done elsewhere. In an attempt to keep a larger share of the profits within their borders, a number of African nations are emphasizing domestic processing capabilities.

In the case of India, there is no domestic presence in lithium refining and processing to speak of, even though there is nascent activity in manufacturing battery packs. In order to be positioned to retain maximal value from its lithium deposits, India should prioritize investments in downstream chemical capabilities concurrently with exploration.

Impact on costs

Given the uncertainty around the economic feasibility of the J&K lithium deposit, it is too early to project its impact on battery production costs in India. All else equal, a domestic lithium source of this scale could meaningfully decrease battery production costs - perhaps by 5-7%.

But “all else” is rarely equal. The answer to the cost question will depend on the lithium concentration within a high confidence interval, as well as the ease with which the lithium metal will be separable from other metals in the deposit such as bauxite. Initial estimates suggest that this deposit features high grade lithium - up to 800 ppm, compared with the 300 ppm considered to be a good baseline - but there are many other variables which may impact where this resources lands on the global cost curve.

Ecological concerns

The location of the J&K lithium deposit, in the Reasi district among the pristine Himalayas, raises key questions around potential environmental impacts of the project. Lithium mining is operationally intensive, requires significant clearing of land, and can leave a meaningful environmental footprint. Much of the Indian union territory of J&K is located in an ecologically sensitive area (Zone IV). And like with any mining operation, it will likely involve some communities being relocated. Though we are years away from any commercial production in the region, some locals in the Reasi district are already sharing their apprehensions about this ‘mixed blessing’.

An Eye Towards the Future

Even as the mining exploration and development process will continue to progress around the world, there is considerable research on novel Lithium extraction technologies. This includes various types of ‘direct lithium extraction,’ which can recover Lithium in higher grades from brines, without needing to evaporate ponds with great resource intensity.

Direct Lithium Extraction (DLE) technologies are in various stages of commercialization (including several that are ‘pre-commercial’) Companies active in the DLE space include some of the world’s largest lithium producers like SQM as well as early stage startups such as Lilac Solutions and Cornish Lithium in the US and UK. It will be exciting to watch DLE’s development through the technological readiness curve even as traditional lithium mining continues to be scaled up.

Thumbnail Image Source: Adobe Stock

*Image Source: EnergyX (https://energyx.com/blog/the-problem-with-current-lithium-extraction-methods/)